Taking Advantage of Growth in Technology – a Venture Capital Strategy

As an asset manager and active LP in Venture Capital funds, we have lots of conversations with other LPs on how to build a strategy in the asset class. We wanted to publicize our thoughts here and are happy to discuss in more detail with whoever might be interested.

Why invest in technology?

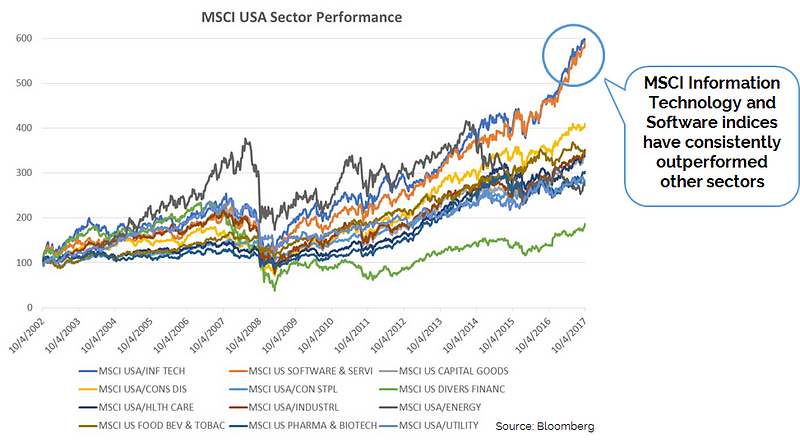

Out of all industrial sectors´ performance over the past 15 years, the two standout sectors has been information technology and software & services, both of which has outperformed against the general industry significantly. This should not necessarily come as a surprise given the growing importance of information technology over a wide range of sectors, from oil & gas industries to consumer products. Furthermore, as a relatively young sector, it continues to grow at a much higher rate than other industries.

How to get exposure: public vs private markets

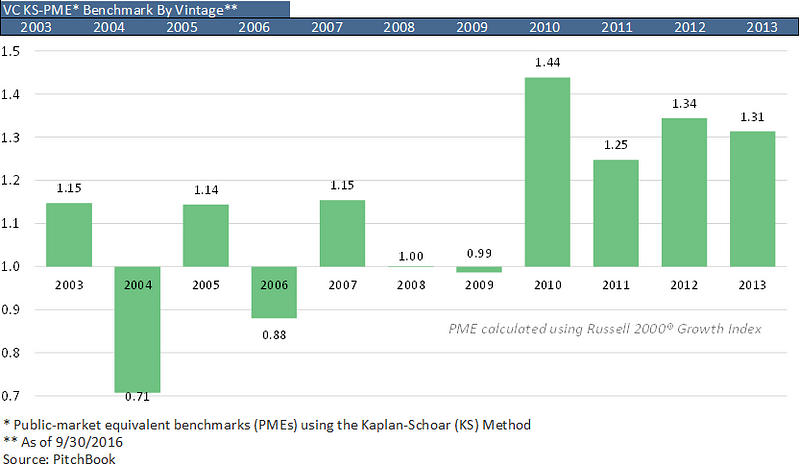

One of the main attraction of investing in private markets is that over the past few years, private markets have outperformed public markets for different reasons. One main reason is purely due to the fact that generally companies tend to go public at a comparatively later stage of growth, and therefore, would usually have a lower scope for growth. Given that greater growth can be expected of a company at an earlier stage, to maximise the benefit from a company’s growth, it makes sense to do it at an early stage, while it is still private. In addition to this, other reasons include the fact that unlike in public markets, private companies have no restrictions with regards to insider knowledge, giving investors a competitive advantage. Lastly, given that private companies are generally thinly traded, there is a lot more scope for an illiquidity premium.

How to get exposure: direct vs indirect

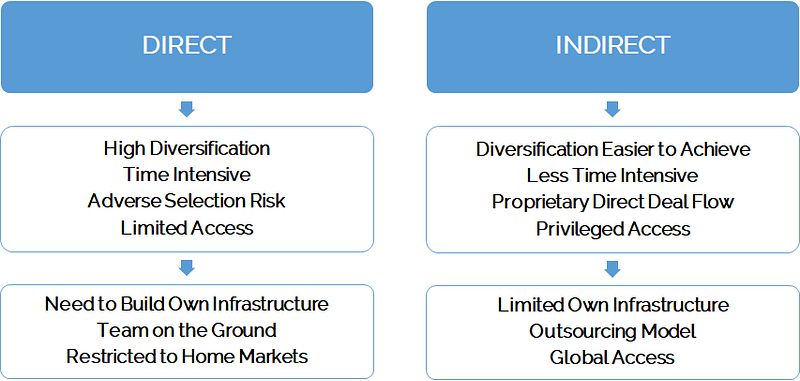

As for the investment itself, it can be divided into two categories; direct and indirect. One main benefit of direct investment is that it allows for a direct interaction with the companies involved, which is highly beneficial if the said investors are well-versed in the field or industry. However, the process is very time intensive and requires the prospective investors to build its own infrastructure to monitor its portfolio, while geographically, the investments tend to be restricted to the nations that the investors are based in.

As for an indirect investment, that is to say investing in other funds or investment vehicles, does certainly restrict the ability of an investor to be involved in the management of the individual companies, there are numerous benefits, whereby it can diversify its investments to different industries, as well as requiring less time commitment and expertise, and most important of all, allows an access to a global market.

As such, for smaller venture capital firms, with a limited manpower and infrastructure, it would stand reason to invest indirectly rather than directly.

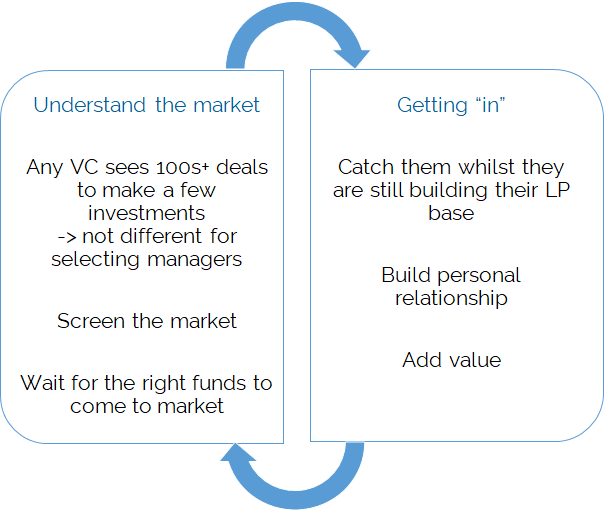

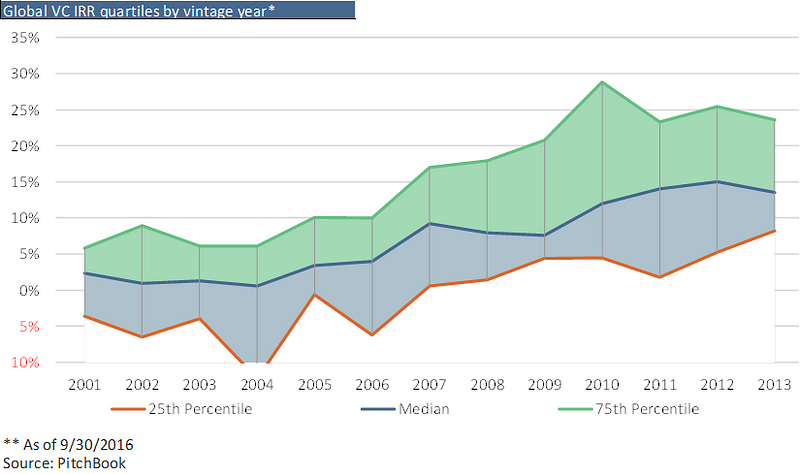

Allocation strategy: VC manager ranking

While for the aforementioned reasons, indirect investment is favourable for smaller investors and does not require the detailed knowledge of individual companies receiving the investment, but there is one significant variable. While the median returns from global venture capital firms have risen, another trend that has been noted is that the return spread between top-quartile and bottom-quartile fund managers have been widening, meaning that it is important to find the right fund manager as well.

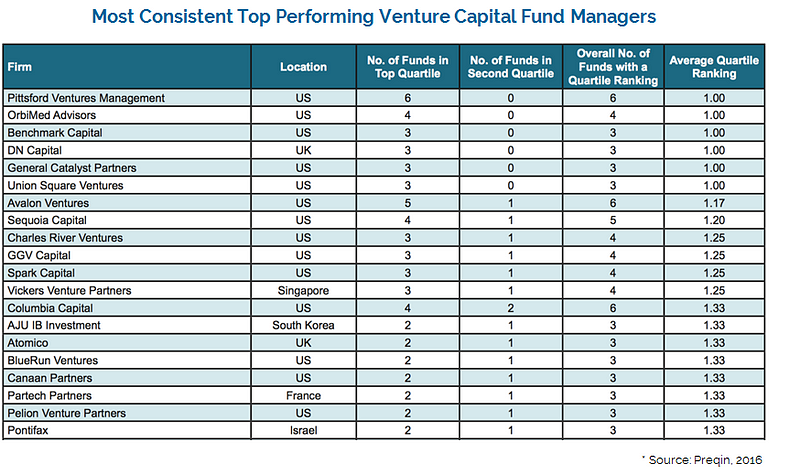

Allocation strategy: top quartile return consistency

As such, finding a top fund manager is of vital importance. And in general, past performance of a fund manager has shown to give a good guide to his future performance. Certainly, this may stand as a testament to the ability of the manager, there are some other factors at play. For example, the brand name of top fund managers are likely to attract more high profile start-ups and founders.

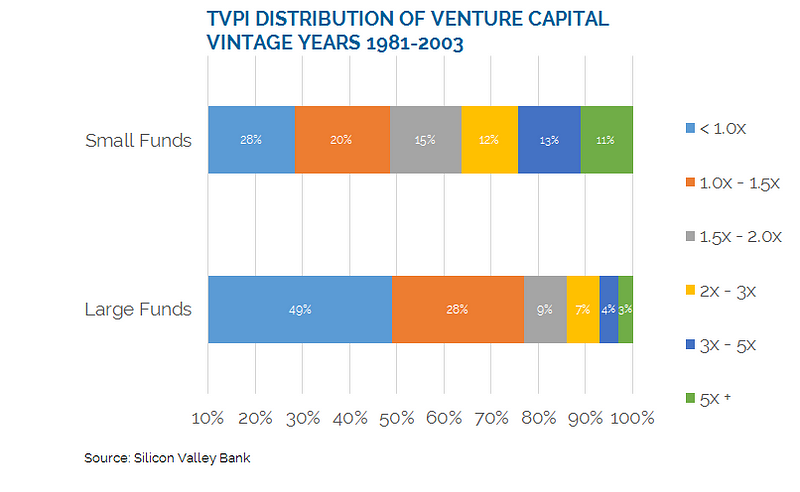

Allocation strategy: small vs large managers

Another aspect of finding a right fund for investment is its size. Historically, smaller funds have yielded better returns. This is due to the fact that smaller funds are more nimble and have smaller portfolio, which means that it is easier for the investor and the fund to have a better alignment of interest, whereas in the case of larger portfolios, the largely diversified portfolio may not necessarily reflect the wishes of individual investors. In addition to this, smaller funds are certainly less reliant on blockbuster exits, as the magnitude of the individual investments are generally smaller.

The case for global diversification

While the US west coast, the home of Silicon Valley, remains as the undisputed hub of global tech start-ups, due to its established ecosystem based on start-ups, there are other regions with growing importance. Within the US, on the east coast, there has been a growing number of healthcare-based start-ups, in cities such as Boston, which can call upon a very large base of scientific institutions.

On the other side of the Atlantic, the UK remains as the leading start-up city in Europe, but with the impending Brexit concerns has shifted the focus towards Berlin and Paris, and there has been many success stories in the past, with the likes of Spotify and Skype.

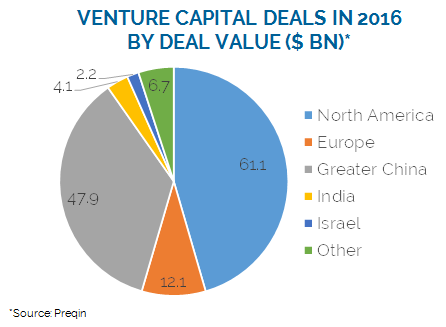

Last but not least, on the Asian sphere, there are three regions of particular interest. Israel, with the number of start-ups in the country being second only to the US, has a good track record in venture capital, with specialties in deep tech sectors such as cybersecurity. On the eastern side of the continent, the two centres of tech investments are greater China and SE Asia. In the Chinese region, the rise of internet giants such as Alibaba and Tencent stand as a testament to the burgeoning tech start-communities in the region, and it’s heavily digitalised infrastructure provide a lucrative market for start-ups. As for SE Asia, it is certainly in its early days in terms of start-ups, given the rapidly developing economies in the region, coupled with large investors in the region such as SoftBank and Temasek, there is a huge potential scope for growth.

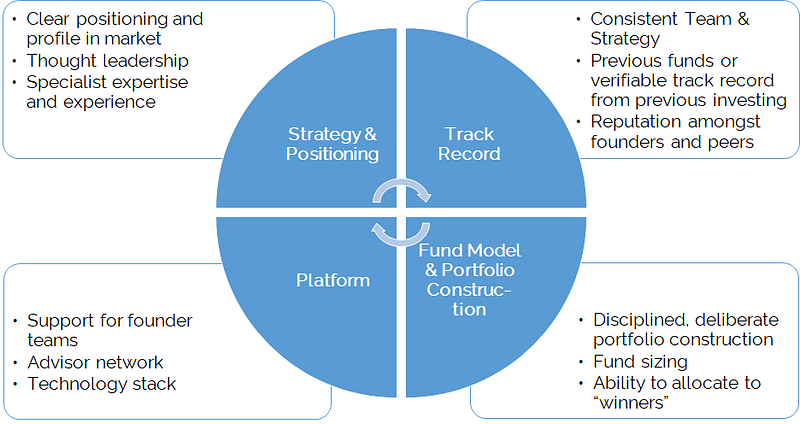

Building a portfolio

From the discussions above, we can therefore start to develop a range of criteria that must be satisfied prior to an investment:

Manager selection criteria

Building a global portfolio