If you are reading this article, you probably already know what Proptech is. You are interested in the intersection of real estate and technology and may be looking to become involved in the next Compass or WeWork.

At Blue Future Partners, we have been investing in both real estate and technology for a while. In this context we have devised an analytical framework within which to evaluate Proptech deals opportunities.

Below graph visualizes the first step of that framework by breaking the PropTech market down into segments (compiled from various sources, see footnotes 1-6):

We then analyze those segments in terms of four categorical overlays (“dimensions”).

The 4 Dimensions of Proptech Start-ups

Looking at the criteria useful for segmenting Proptech startups, we narrowed down four key features that differentiate companies in this space:

- End user2: Is the service/product provided addressed to consumers or enterprises?

- Process3: Within the value chain of real estate, which activities does the service/product cover?

- Technology3, 4, 5, 6: What types of technologies are involved?

- Level of asset ownership: How deep is the level of ownership in the asset itself?

Residential VS Commercial2

Within this model, the first dimension involves differentiation between startups addressing the residential and those addressing the commercial real estate market. For instance, while easyProperty helps consumers to sell their houses, Squarefoot supports companies looking for an office.

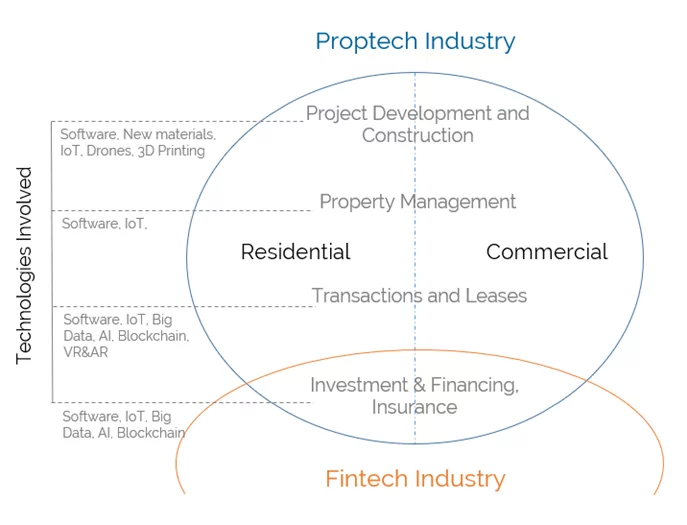

Process within the Real Estate Value Chain3

The second dimension looks at process. The real estate value chain can be broken down into four macro-processes3: Project development and construction, property management, transactions and leases, and real estate investing, financing and insurance.

These processes also refer to the “life cycle” of real estate assets: first a property is designed and built, then managed by the owner, and finally sold and/or rented with financial resources.

Clearly, as the graph above suggests, there is an intersection between Proptech and Fintech markets1, 3 ,4: Indeed, finance is a fundamental underlying aspect of real estate.

Elaborating on different Proptech maps we found in our research1,2,3,4,5,6, we segmented the Proptech space according to the different processes in the real estate value chain below:

Technological impact3,4,5,6

The third dimension concerns the impact of technology on the underlying real estate assets. Academics and professionals distinguish between three waves of Proptech that have different applications4,5,6.

We have summarized in the chart below which real estate process each new type of technology will impact the most3,4,5,6.

Level of asset ownership

The fourth and last dimension is probably the trickiest one. Startups can be differentiated by the level of direct ownership of the underlying real estate assets as part of their business model. We can therefore divide companies in two categories:

- Startups with a low level of real estate assets owned

- Startups with a high level of real estate assets owned

For instance, a company such as Airbnb, which does not own the properties offered in its marketplace, has a low level of assets owned. Opendoor, in contrast, has a high level of assets ownership, as it purchases properties outright to sell them later.

This differentiation is fundamental as investing in companies with a high level of real estate assets means to invest not only in the company, but also in the value of the assets.

A simple example

If we look at a company such as WeWork, for instance, we could easily position it following above analytical framework:

- End user: commercial

- Core Processes: Construction + Transactions & Lease (Long term/co-working spaces)

- Technology: simple renting platform (e-commerce software)

- Asset Ownership: High

In this way, Proptech companies and verticals can be easily described.

Conclusion

Will the co-working spaces of the future have a high-level asset ownership? Or will they be VR powered digital spaces with no assets involved? Are property search services moving from low to high levels of asset ownership? Will AI impact most residential search services or investments?

These are clearly complex questions that future Proptech innovators will have to address.

The above analytical framework has proven a useful tool for us in evaluating deal flow in the context of our own value add, expertise and investment strategy in the Proptech space.

Sources:

- PropTech: What is it and how to address the new wave of real estate startups?,0, Vincent Lecamus, 11.07.17, https://bit.ly/2CXdZlN

- Real Estate Tech Market Map, The rise of Real Estate Tech, CB Insights Research Briefing, 18/10/18

- The Growing Influence of Proptech, JLL, Tech in Asia, 04.18, https://bit.ly/2Rt5eUL

- PropTech 3.0: the future of real estate, University of Oxford, Andrew Baum, April 2017, https://bit.ly/2pBaNE0

- Here are the 5 most well-funded proptech startups in Asia, Tech in Asia, Daniel Tay, 09.07.18, https://bit.ly/2yc9Ky8

- Proptech 3.0 and the rise of Crypto Securitization of Real Estate, io, Andre Lopes, 19.12.17, https://bit.ly/2O3mp1c